A discussion with Alastair MacLeod and Wayne McGauley about the importance of After-Tax returns and what the key attributes of a tax-effective fund are.

Alastair MacLeod, Portfolio Manager, explains his thoughts on why markets are at a tipping point, his views on how this tipping point is a regime change for investors and the

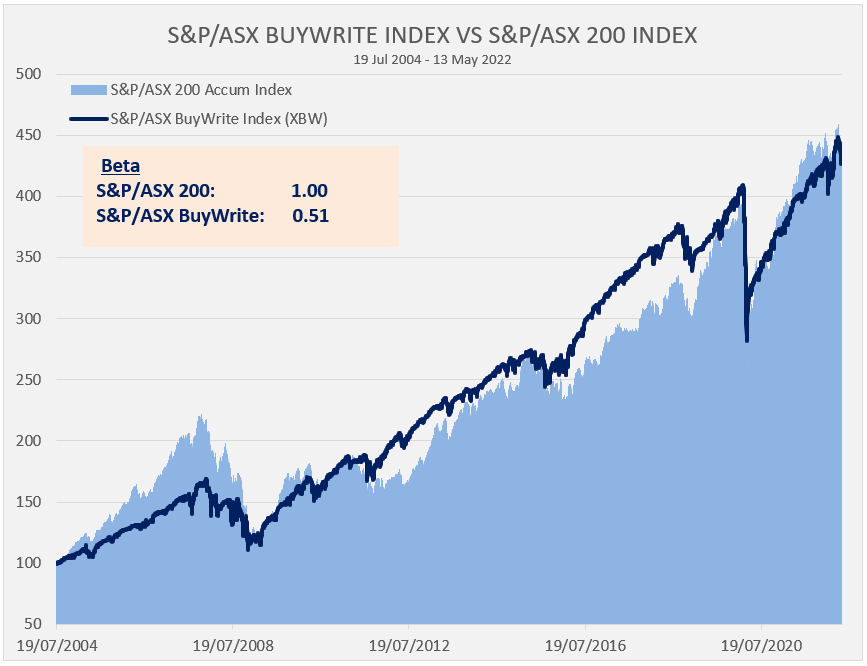

It goes without saying that protective strategies need to work in bear markets – but a review of three traditionally defensive strategies during the past two major drawdowns shows very

As market returns trend lower, many investors are waking up to the underlying risk in their portfolios. In recent years as interest rates have marched steadily towards zero, investors who

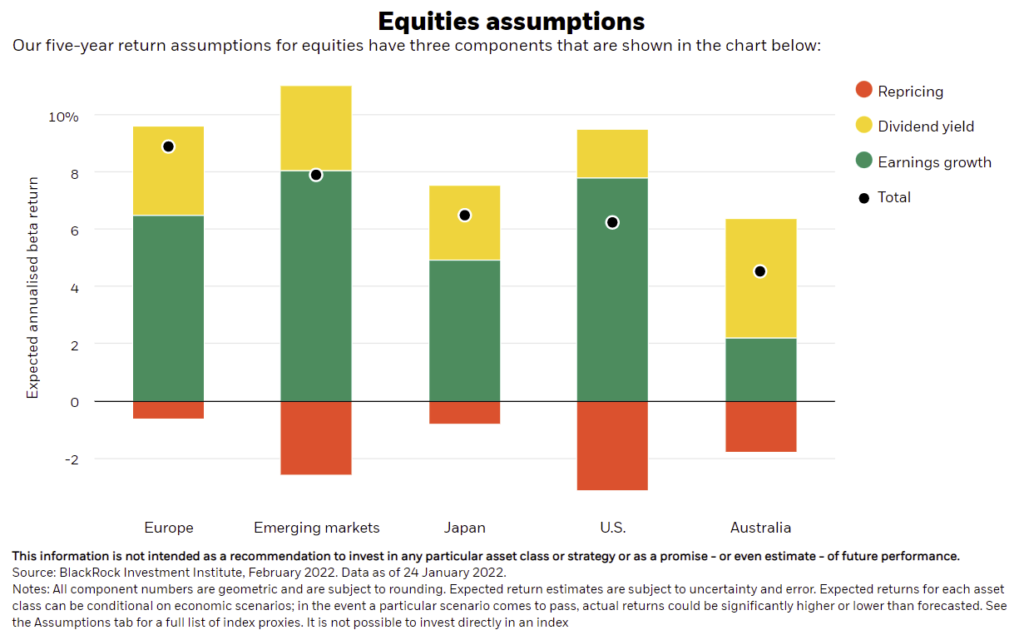

Australian equities are likely to underperform the world market over the next five years, according to the Blackrock Investment Institute. Local market returns are expected to average 4.5% over these

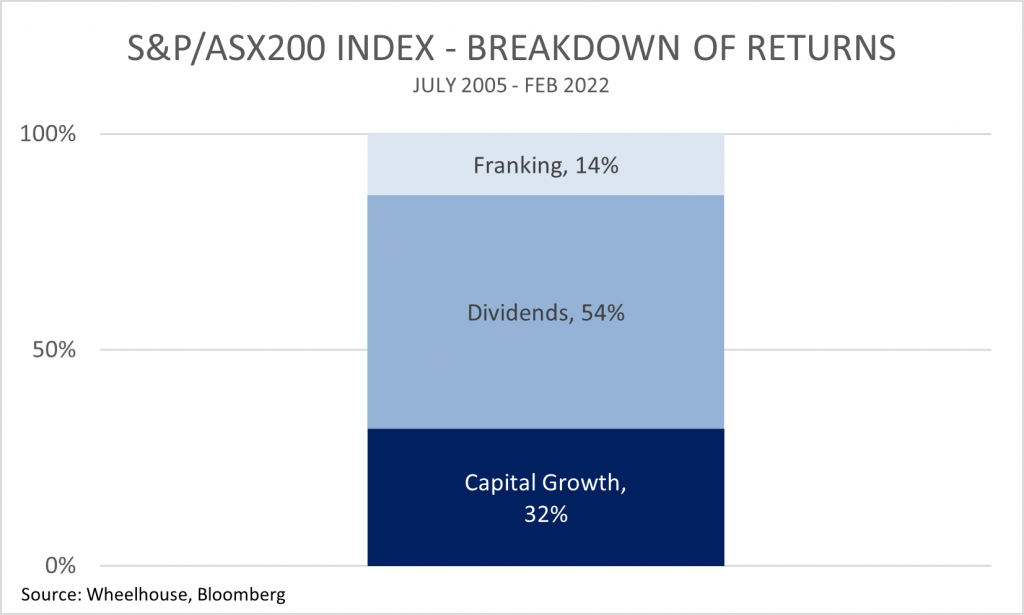

It’s no secret that Australian investors love their dividends. But recent Morningstar research has found that a portfolio of higher dividend-paying shares actually meaningfully outperforms over the long term. But

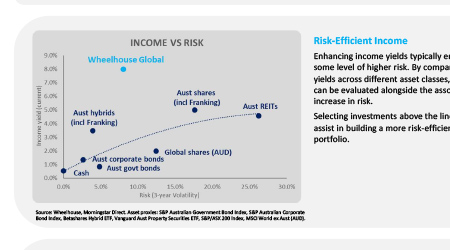

Meagre yields from cash/bonds have left many investors reducing their usual weights to these defensive assets insearch of more acceptable returns. Investors have been pushed further along the risk curve

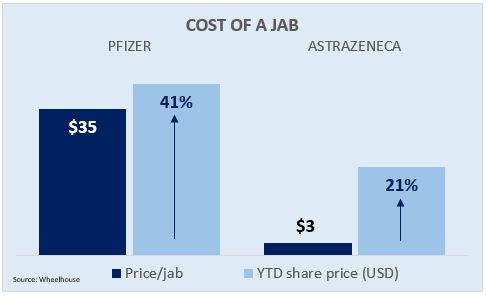

When receiving my jab last month (thankyou nurses at RBWH in Brisbane for your excellent care!) I couldn’t help wondering how much all these vaccines were costing. From a purely

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.OkPrivacy policy