Texas hedges

Continue readingTexas hedges

Continue reading

Dear fellow investor,

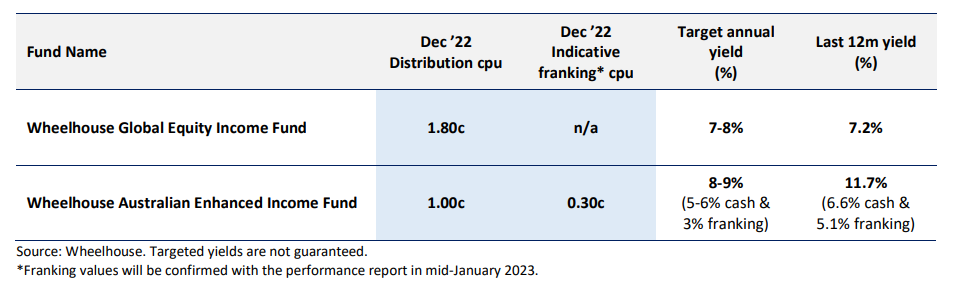

We are pleased to advise that the Wheelhouse funds will pay the following distributions to investors for the

quarter to 31 December 2022.

The funds’ unit prices on the 31st December will be adjusted for the cash distribution amount above. Franking is not included in the unit price so there is never any adjustment for franking.

The monthly newsletter and performance reports for both funds will be published by mid-January.

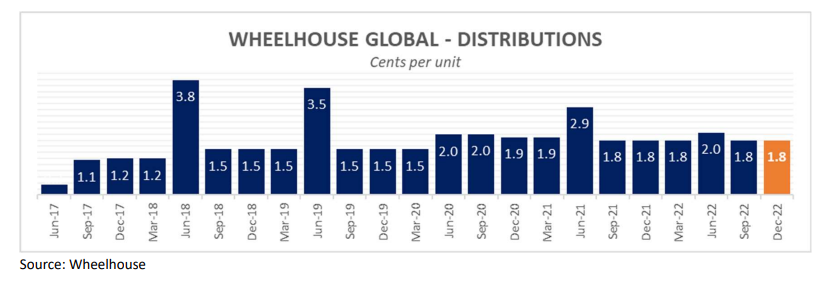

The December 2022 distribution marks the 23rd consecutive quarterly distribution from the fund which has consistently met its targeted 7-8% annual income yield. Cumulatively since inception, the Fund has yielded nearly 42% over the roughly five-and-a-half-year history.

The Global Fund’s distribution is almost entirely comprised of income with minimal capital gains distributed. This income-based distribution is by design, to ensure the distribution profile is sustainable even during periods when realised capital gains may not always be available.

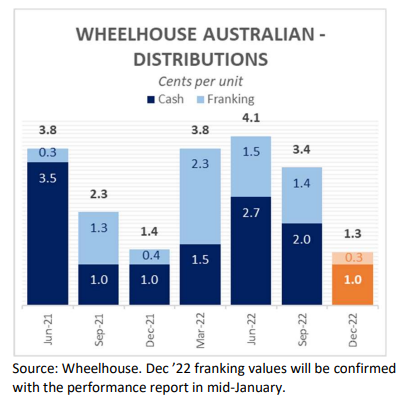

The Australian Fund has also met its distribution targets of 5-6% cash, plus around 2x the franking of the broader market (S&P/ASX200 Index). Franking generation has actually been nearer 3x the market since inception, although looking forward we believe 2x is a more realistic expectation.

A unique characteristic of the Australian Fund’s strategy is that it designed to capture around 2x the fully franked dividend yield of the market, which along with received option premium, underpins the quarterly distribution profile. With essentially zero turnover, we anticipate there will be minimal realised capital gains to distribute in a typical quarter.

Income has always been an important part of the total return of all our investment strategies.

Income helps us to reduce risk, reduce reliance on capital growth, and is the bedrock for our investment approach of maximising returns for a targeted level of risk. Should capital growth be more challenging in the months and years ahead, we believe the real return characteristics of income will serve us well across both strategies.

For our Global fund, this past year was another milestone in demonstrating the defensive characteristics of our investment approach across a completely different set of investment conditions. In every drawdown since inception, the fund has delivered on its defensive objectives regardless of environment or circumstance.

We’ll provide a more thorough performance update and outlook for the year ahead in our monthly newsletter, published in mid-January.

On behalf of the team at Wheelhouse, I would like to thank you for investing alongside us during 2022. Over the past 12 months we welcomed many new investors to our unique risk-targeted approach to investing and we look forward to engaging with our investors more regularly during 2023 with the recent engagement of Wayne McGauley as our Head of Distribution.

We look forward to our continued partnership and wish all our investors a safe, healthy and prosperous 2023.

Yours sincerely,

Alastair MacLeod

Managing Director